Certain numbers are very important in our lives. If you're on a diet, you'll tend to monitor the digits on your scale with a mixture of hope and trepidation. Prospective college students who've recently taken the SAT wait with bated breath for the numerals that comprise their test results to arrive in the mail. If you're in the process of seeking a car loan, there are three digits that matter most: the trinity of numbers that comprise your credit score.

A credit score is a reckoning of an individual's creditworthiness based on an analysis of the data reflected in his or her credit report; this number provides potential lenders with the means to evaluate credit risk quickly and in a relatively objective manner. Your credit score helps determine the interest rate you will pay on your loan, and whether lenders will want to grant you credit to begin with.

To arrive at the score, values are first assigned to the variables contained in your credit report; mathematical processes then calculate the all-important number, assigning each variable a weight that reflects its relative importance. The most commonly used assessment is the Fair, Isaac & Co., or FICO, score.

As would be expected, your payment history has a big impact on your credit score. However, it's not the only factor that's considered. (Photo by Ronald Montoya)

For many years, credit scores were kept secret from consumers, available only to prospective lenders looking for a way to size up potential borrowers quickly. That has changed. Under pressure from consumer groups, Congress, state legislatures and leading lending institutions like Fannie Mae, FICO has made credit scores accessible to consumers. Additionally, information is available that sheds light on how this score is determined. While an exact breakdown of the formula used has not been revealed, it's now possible for consumers to gain some insight into what factors impact their score.

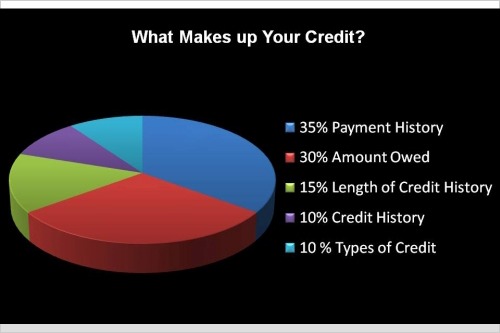

Five factors play a part in FICO's score calculation: payment history, outstanding balances, length of credit history, new credit and types of credit used.

Payment history. Your payment history impacts about 35 percent of your total FICO score. Details regarding payments made on credit cards, retail charge cards, installment loans and mortgages play a part here. How timely have your payments been? How much do you owe? If you've made late payments, how recently did these payments occur? If you've got few or no late payments, your score will be improved. Also, recent late payments will hurt your score more than those made years in the past.

Outstanding balances. About 30 percent of your score is impacted by the amounts you've got outstanding to creditors. Owing a lot on many accounts won't necessarily hurt your score. If you're at or near your limit on your credit cards and other "revolving credit" accounts, though, your score will be compromised.

Credit history. The length of your credit history determines about 15 percent of your score. If you're just starting to build your credit history, there's not much you can do to improve your standing in this area over the short term.

New credit. New credit acquired determines about 10 percent of your score. Applying for a slew of new credit is one of the easiest ways for people to mar their rating. The FICO model evaluates how many new accounts you've established, how long it's been since you've opened a new account and how many recent credit inquiries have been made by credit reporting agencies. Self-initiated credit report requests will not impact your score.

Credit type. Ten percent of your score hinges on the types of credit you use. What matters here is your mix of installment loans, mortgages, retail accounts, credit card and finance company accounts. According to FICO, this factor is given less weight if it has full information on you regarding the other four factors.

Now that you know what goes into calculating the numbers, here's some information about the scores, and what the numbers actually mean:

According to FICO's Web site, FICO scores range from 300 to 850. The higher your score, the better your chances for getting optimum rates on your loan.

A credit score of 720 and above is considered excellent; those who score within this range have the easiest time obtaining loans, and get the best rates.

Many lenders consider a score of less than 620 subprime. Subprime borrowers may still get loans, but face higher rates than borrowers with higher credit scores.

Different lenders have different tiers; shop around to make sure you get the best rate.

Remember, knowledge is power when it comes to getting the best deal on your car loan. If you're a prime borrower who, out of ignorance, has applied for a car loan with a subprime lender, chances are you won't be told that your credit score allows you to obtain a much cheaper rate with a prime grantor. Thus, it suits you to know where you stand score-wise, so that you may target appropriate grantors in your search for a loan. You can get an online credit report by visiting the Web sites of the nation's three credit bureaus: Experian, Equifax and Trans Union.

.